Preview:

John Fuller: This is Focus on the Family, and our guests today are Brian and Cherie Lowe. Here’s Cherie reflecting back on how they dug themselves out of a tremendous amount of debt.

Cherie Lowe: And then it dawned on me that we had paid off $127,482.30, 19 cents at a time. Because we had learned to say no to 19 cents. And if we could say no to 19 cents, we could say no to $1.90. We could say no to $190. We could say no to $1900. Because learning to say no is really the most effective way to pay off debt.

End of Preview

John: Hmm. Well today, we wanna come alongside and give you hope to do just that, to say no. Uh, with hard work and determination, you can pay off even huge amounts of debt. You host is Focus on the Family President and author Jim Daly, and I’m John Fuller.

Jim Daly: John, what I love about Brian and Cherie is their honesty and relatability. They shared last time that they had accrued over $127,000 in debt. Credit cards, student loans, medical bills, things like that. And not the fun stuff like vacations. And their journey to pay off that debt began with Brian, and through that gentle encouragement and some vision casting, Brian eventually, after two years of wresting internally about this, was able to get Cherie on board. And, you know what? Here at Focus on the Family, if you’re a couple that’s struggling in this area of finances, we wanna help you. Don’t be embarrassed to call us and get to the resources or the tools to help you do this better. Don’t wait two years to begin to address it. Let’s work together to get you in a better place today.

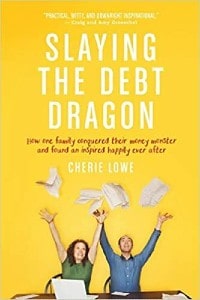

John: Hm. And our number here is 800, the letter A, and the word FAMILY. We’ve got Cherie’s book called Slaying the Debt Dragon: How One Family Conquered Their Money Monster and Found an Inspired Happily Ever After. We also have this conversation on CD. We began last time, uh, with a pretty crucial framework for you to understand where we’re at in today’s discussion. Uh, you can get the full download instantly or, uh, listen on our free app. We’ll have details at focusonthefamily.com/broadcast. Now the Lowes have two girls and Cherie is a writer and, uh, has a very popular blog called Queen of Free. And this conversation was recorded a number of years ago when their girls were younger. It was really popular. And we’re bringing it back today to help you as a family. Here’s how Jim started day two of the conversation.

Jim: Brian and Cherie, last time we left off, uh, and we were talking about how the two of you began to tackle your debt. And I wanna hear more about that today. But I’m curious how did this affect your children? Um, how old are your daughters right now?

Brian Lowe: Right now they’re 13 and seven.

Jim: So you’ve done this over the last how many years?

Brian: Well between, uh, April 2 of 2008 until just before that in 2012 was the journey of paying off the $127,000. So they were much younger then. And it’s real easy to take a look at that number and think that that just happened overnight. But we had a child go from birth, because she was born right before that began, un- into a, a child that was reading, literate. Uh, so four years is a rather long time of day-to-day stuff. But they were definitely a part of the journey. And I, I’m confident that you need to make your kids part of the journey in an age-appropriate way.

Jim: How did you do that?

Brian: Uh, one of the ways that we did it was explaining what we were doing, especially our, our oldest was rather articulate and, and so we would explain what we were doing. We would set small short-term goals. You know, here’s what’s happening. Uh, it’s sort of the monster under the bed theory. If you don’t ex- explain to the kids what is happening with the money, they’re going to make something up. Uh, they’re going to make something up and it’s going to be fearful and frightful. You may think you’re having conversations in private, but your kids know. Uh, they know if you’re stressed out over money. They know if you’re fighting about money. They know if money is tight. Uh, but it will be the worst-case scenario in a child’s mind. So explaining it in a very practical, pragmatic way to your kid, and an age-appropriate way, is the best way to go.

Jim: Let me ask you this, uh, you know, for that honesty factor. I mean, some children, uh, they’re gonna see something or their friends will have something and there can be, you know, tremendous disappointment that they know- maybe even, uh, guilt on their part that they can’t ask you about it ’cause they know you can’t afford it. Did you ever have that kind of experience? Or maybe through your blog, Cherie, did you ever have parents express that? That, you know, many of us as parents, we overindulge our kids-

Cherie: Mm-hmm.

Jim: … right? And that’s the bottom line.

Cherie: Oh yeah.

Jim: Because it brings joy to them to see them, uh, have or do the things that they like to do. And so we-

Cherie: Mm-hmm.

Jim: … we’re kind of s- we spoil them in that way.

Cherie: Definitely.

Jim: When we’ve gotta say no, um, some kids can be really disappointed. How do you handle that emotion as a parent when they’re- they’re so disappointed that they can’t do that thing or get that thing?

Cherie: So to begin with, I always encourage people that that desire and that longing to give good gifts to your children, that is a mark of the image of God on your heart. And He longs to give us good gifts as His children. And so that we would want to turn around and do that for our children is just a natural way that we have been divinely created.

Jim: Mm-hmm.

Cherie: And I love that.

Jim: That is good.

Cherie: At the same time, it can turn into a weakness if we’re not careful. And I think that idea of sacrificing something for a long-term goal really can translate to kids. And I tell a story in particular in the book about our oldest daughter, Anna, who’s now 13. But she was seven at the time. And we were in a very large retail store with a red target, uh-

Jim: (laughs)

Cherie: … that bullseye store. And she had found a toy in particular on the shelf that she wanted really bad. And she looked at it and she said, “Mom, you know, I really want this. But I know we’re working to pay off the credit card bill.” And we had allowed her to choose what we would do to celebrate that. And that was to go to a local, um, theme park, water park, indoor water park. And she said, “I want this toy, but I wanna go to the water park more.” And she put it back on the shelf. And I did, like, looked around. Like did anybody else see that.

Jim: Yeah (laughs).

Cherie: Like this is so-

Jim: That’s my girl.

Cherie: … exciting. And to help them along that journey of realizing to have something else, sometimes we have to say no to smaller things, I think is just a lesson all of us need to learn. I wish I would’ve learned it earlier in my adulthood even. But I think you can help captivate their heart. We also try not to use the phrase we can’t afford that. Um, because it creates this sense of scarcity.

Jim: Right.

Cherie: So it may be more along the lines of we’re choosing not to do that right now instead of we can’t afford that, which can become kind of a real negative thing. We’re choosing to do this instead.

Jim: Right. I like that. That we’re choosing this over that.

Cherie: Mm-hmm.

Jim: Uh, talk about, and you’ve mentioned it a couple times here, the Queen of Free, your blog. I love that title. Um, what is that about and what are some of the, uh, I guess inquiries or dialogue that’s taking place on Queen of Free?

Cherie: Yeah. So queenoffree.net I set up back in 2008 just as we began our journey, mainly because I love free things.

Jim: (laughs)

Cherie: And sounds a little shallow. But ever since I was a little girl, I had this book where you could write away and send a self-addressed stamped envelope, which no one does anymore. But they would send you free items in the mail. And I began to find free things online. I’m very good at it. And I would email friends and family and tell them, hey, you can get free tea at Chick Fil-A today. Or there’s this great coupon at the mall that gets you something else for free. And inevitably I left someone off the email list. And they would say, oh, I wish I would’ve known. And I began the website kind of as a clearing house for people to go there. And over the years, it’s developed into a community where I’m able to share not just free items but frugal living tips, wisdom when it comes to money, parenting and marriage ideas as it comes to paying off debt and what it looks like, um, to live intentionally with your finances. So it’s been fun. And I- because of that, I’ve gotten to speak to a lot of people, hear their stories, and be just as encouraged by their process of paying off debt as they were by ours.

Jim: Well, and it sounds like, uh, you know, an important factor of getting out of debt and living well on a budget is, uh, support groups. And that leads to the other point. Uh, with friendships, that could be a bit of a strain because your friends may wanna do things and you’re thinking, okay, that wouldn’t be the way I’d spend $100.

Cherie: Mm-hmm.

Jim: And so we’re not gonna be able to go with you this weekend. What did you do in that friendship space in order to make sure that your friends were supportive of what you were doing?

Brian: Well again, like Cherie talked about earlier, that bringing the darkness into the light and the darkness loses its power. We had told our friends what it was that we were doing. And I’m sure they did awesome expensive things. But we weren’t asked to be a part of that. They knew what we were doing, and they loved us enough not to try to bring us into the mix on that. I- what I would encourage people to do if they’re in that situation is to get better friends. Uh, and-

Jim: Well, I was gonna say-

Cherie: (laughs)

Jim: … did it- did it change your relationship with them at all?

Brian: It, it- I think it, it built community. We are made for community. You know? Uh, God is community. And our relationship with God is part of that community as well, and our outreach to others, uh, is important. And we have a great community group that we’ve led for about eight years now. And they’re fantastic. And the- one of the most amazing things that happened, and I’m, I’m not a weeper. Uh, but when we paid off all of our debt, uh, at our small group meeting that evening, there was a cake and some sparkling cider. And the cake just had the word freedom written across it. And, and our, our group knew how important it was to us. It inspired some of them to go through a similar journey as well. And they are now free from the chains of debt also. Uh, so you go through that together and you bring other people along with you. It’s important to have a support network and community. It’s also important to have people that are going through the same journey as well-

Jim: So you can talk together-

Brian: So you can talk about some of the similar struggles-

Jim: Problem solve-

Brian: Uh, problem solve-

Cherie: Mm-hmm.

Brian: … together.

Jim: Let me ask you this. The, the end of this journey now, the end of the road, uh, put you in a better place. Talk about, uh, the ability to give in the name of the Lord. The ability, that freedom that you talk about. What’s the environment like today compared to 2008 when you saw this mound of debt? Um, what does that freedom look like?

Cherie: So much fun (laughs).

Brian: It’s a lot of fun.

Cherie: It’s so much fun. We sat down. We’ve been mentoring a couple for the last three years who just got married this summer. And we put a rather large amount of cash into an unmarked box and handed it to them at dinner. And I thought that they were going to just lose it there in the restaurant. And we just kinda were like, yay, this is so much fun. And that’s- couldn’t have been possible if we hadn’t paid off this debt. And not just giving to the local church and to ministries that we call, you know, feel strongly called toward supporting, but those little things like buying somebody’s groceries at the grocery store-

Jim: Ah-

Cherie: Or, you know, doubling the amount on the bill at the restaurant to, you know, encourage a young person who is waiting on us. Those things have been, for me, some of the biggest blessings and the most fun things that we’ve done since paying off debt.

Jim: I, I think that’s beautiful and that really does put you in a more generous mood, right, then when you have the ability to do it. Have your daughters picked up on that? I, I’m sure they’re watching this and seeing this now that they’re teenagers and they’re going wow.

Brian: Th- they have and it- and it’s just a part of their life. You know, your kids are going to learn about money from you whether you’re good with it or bad with it, whether you’re generous or not generous. They learn by watching. Uh, more is caught than taught. And it’s not a surprise to them if we pick up somebody’s bill at a restaurant because they’re in fatigues or because it’s a single mom. Uh, or because we just want to. This isn’t a big deal for them. And occasionally our eldest will kinda look at me. And we don’t even communicate with words-

Jim: Right.

Brian: And she just knows, just go ahead and take care of that. We have a- an entire budget, um, that is just- it’s not an envelope. It’s an online savings account. And we have nicknamed it. And- because we can do that with our bank. Nicknamed it generous. Uh, and, uh, that’s awesome. And Cherie and I will communicate back and forth just to make sure that we know how much is in there. If we see a need or know that somebody is, uh, going on a mission trip or trying to do something different, that we can communicate with one another about how much we want to give and we have that ability to do that.

Jim: No, I think that’s wonderful. And that is really the upside of the discipline that you’ve done over these last many years. I mean, this is where it does become fun, huh?

Cherie: Mm-hmm. And we’ve done other fun things too. We’ve gone on vacation as a family. Some of those things that we gave up while we were paying off debt, we’ve been able to do for ourselves. But I think, again, it’s always more blessed to give than it is to receive.

Jim: That’s a good point. And I mean it really is a good point because you can get overwhelmed. And I was gonna ask about that. And Cherie, with your blog and the people you counsel, uh, the attrition factor here. You know? Uh, of course usually the first of the year people are starting and maybe by February/March, they’re done ’cause they just can’t get the discipline of it. Speak to that couple, maybe young couple, maybe an older couple-

Cherie: Mm-hmm.

Jim: … uh, and they’ve started with good intentions but two to three months into it, they’re not staying focused and they’re not achieving it. So rather than fight through that, they’re, they’re thinking about bailing out. What would you say to them?

Cherie: Well, author John Trent has this great idea of the two-degree difference. And that is that if we make small change over time, it adds up. And that’s much more sustainable than making a rapid change overnight. And we know this. If you try to change your habits toward exercise or nutrition or even disciplining your kids, if you make too hard of a change, then you’ll fall off the wagon. It will not go well. I always use the example of if you’re a diehard Diet Coke drinker and you say, you know, tomorrow never again, as long as I live, I’m never gonna drink it again. And then by the end of the week you’re probably going to be sitting in a, you know, mass of cans smashed on the floor-

Jim: (laughs)

Cherie: … in some sort of saccharin, you know, sort of driven experience. But it’s just not sustainable. You have to gradually move toward that change and pick one thing, one area, to focus on to begin with. So we didn’t do everything overnight. I didn’t get up the next morning and say, okay, now I’m gonna make my own laundry detergent. And now we’re gonna, you know, call the companies and change our billing. And we’re gonna do all these tomorrow. Instead, we took small steps of obedience in the right direction. And you’ll find that once you find some success, that motivates you toward making more sacrifices or just looking at your money differently.

Jim: And Brian I so appreciate the openness about not eating out and that was a commitment you made to the family. And for two and a half years you didn’t do it. Um, certainly for Jean and I, when we look at our budget, that’s- that’s an area where for us, we’re both always concerned about. ‘Cause we’re on the go so much. We’re traveling a lot together. And eating out just becomes a way of life. But when you look at it, I mean, I was thinking the other day a fast food stop for my boys and I was, like, $23. And it caught my attention. This was like for a breakfast sandwich for all three of us. And I was thinking this is ridiculous. But it adds up, doesn’t it?

Brian: It does add up. And for me it wasn’t about a morning muffin as much as it was a leadership issue. And leadership comes in a lot of different forms. And I think it’s real easy to try to, uh, use your words to lead as opposed to using what you do day to day to actually lead your family and lead it well. We had this big journey. And I had cast this vision long. So for me it was all hands-on deck, anything you can do to try to defeat this dragon. And if that meant cutting back at restaurants, then that was something that I was going to try to do. It wasn’t actually the first time that I had tried that two-and-a-half-year stretch. I had; I had tried to go just 30 days. And I think I, I made it a New York minute. Uh, there was some-

Jim: (laughs)

Brian: There was some bagels at church. I’m not even a bagel fan. But they were there. And, and I just forgot. Uh, but then the-

Jim: (laughs)

Brian: … the next stretch… It took about 40 days or so. Uh, it- for kinda the desire and the habit of, of going to restaurant to go away. And 90 days when I just didn’t even care. Uh, and that was- that was a pretty easy fix over time. And I set these arbitrary rules, uh, for doing it. So there was nothing, even if it was free. So if, uh, the folks that I worked with were bringing in pizza, I wasn’t gonna have it. If it was water, I wasn’t gonna drink it. Because you have to set that line somewhere. You know, if it’s an illegal substance and you have a problem with an illegal substance, if it’s free, it’s still an illegal substance. It doesn’t change the nature of it. And I had a problem with eating out at restaurants. And so I treated it like an addiction. And that helped. And because we were spending that much money less, anything, or anywhere where we saved, it went toward the goal of paying off debt.

Jim: So to, to make that step doable, ’cause some people are going oh my goodness. That’s- ugh, that’s ridiculous. But to make that step doable, you had suggest- I’m hearing you suggest aim for 30 to 40 days and just give that a run, even if you stumble a bit. Restart the clock, get to 30, 40 days and you’ll find out how irrelevant it becomes.

Brian: Well w- with any change its day to day. You know, start with today. And then tomorrow is yet another day. Uh, and each day after that you just keep going. And then eventually it just becomes a crazy streak. Uh, and then you don’t wanna break the streak and it keeps going. I found it actually harder to give that up than I thought it was going to be, to actually eat at a restaurant again. The funny thing was, you know, re- restaurants are great. And they’re, they’re convenient. I’m not knocking restaurants. But, uh, that first meal back was amazing. The second meal was really good. The third meal was great. But after that, everything just tasted the same.

Jim: Uh-

Brian: Um, so I think we, we get induced by the convenience of it. And really, if you think about the time that you spend going somewhere, you could do most of that at home.

Jim: Eh- again, great advice. Uh, talk about the difference or the attributes, I guess, the character, the Godly character of contentment and gratitude ’cause that’s a big part of the book as well-

Cherie: Mm-hmm.

Jim: Um, in this environment where you’re smothered with debt, it’s hard to have those attributes, isn’t it, to be grateful and to have gratitude toward the Lord for your environment, for the house you live in, for the car you drive, for whatever it might be.

Cherie: Right.

Jim: How do you- how do you develop a, a stronger heart of gratitude and contentment?

Cherie: So one of the things you need to do is control your influences a little bit. And I can remember struggling deeply when we were about two years into the journey and turning on my computer and signing on to social media and beginning to see how everybody else had an awesome life. And I was at home in a stained t-shirt and gym shorts that I’d had since college. And, you know, it was one of those situations where I thought everybody else is out for dinner. And everybody else is having an awesome vacation. And here we sit. And God, do you really care that we’re making these sacrifices? And then I began to reflect on the really good things that had happened that week. That our daughters had played in the sprinkler. And that sprinkler Brian had made out of PVC pipe, was worth more to us than a trip to the water park. And that, you know, I love iced tea. That’s like one of my favorite things. And I can make that at home, and it doesn’t cost me hardly anything at all.

Jim: It probably tastes better too.

Cherie: I think so too.

Jim: (laughs)

Cherie: I totally think so. So, you know, I began to just count those blessings. And I will say that gratitude fights off those give me feelings, that temptation of greed. It is the opposite. And if you can fill your heart up with gratitude and you begin looking around your house and think, well, we have so much stuff that we make a trip to Goodwill to get rid of our stuff. You know? We have so much already. And that’s an essential part of the journey too. It’s not as glamorous. Everybody loves when you pay off the debt. Nobody thinks about those days in between necessarily. But we know that, you know, that ending will be a blessing because you started, and you did the difficult things.

Jim: You know, some of us are motivated by that finish line. And you’ve talked a little bit about what that finish line looked like. But give us the emotion of that day. And take us through what happened when you finally paid it off. I mean, I’d probably be burning things. I mean, like, you know, the payment due notice or something like that. What did you do to celebrate that day?

Cherie: (laughs)

Brian: Well, we knew it was coming. And- because we, we had it within about 30 days that we knew just based on what we had been doing, it was going to happen. Well, it turned out money came in early. Uh, and Cherie actually didn’t know. And, um, and so I had- I had money in my hand that was enough to pay off the debt, the last of the debt. I would write it on post-Its, um, periodically, how much that we owed. And scratch it off until I ran out of the post-It. I’ve still got the last post-It note in my office with the amount that we paid off that I keep. And so I went to the bank, made a deposit. Because both of us are so financially involved, we checked the bank account probably more regular than healthy people should. (laughs)

Jim: (laughs)

Brian: Uh, but, but we- so I knew that Cherie would know that there was a deposit that was 30 days ahead of time, unexpected, but I wanted to surprise her with this good gift. So, uh, basically I just left work. Uh, I, I left work. I went to the bank, made a deposit. Cherie had gone, uh, without things, uh, for some time. Uh, and I went, and I basically just bought her, uh, a Hanes five pack. Uh-

Jim: (laughs)

Brian: … and, you know, no- nothing weird or extravagant or anything like that. Uh, but I had known she had gone without. And, you know, we had made sacrifices. And it- I just wanted it to be kind of this moment. This, uh, a very odd Ebenezer Stone, uh, where we could say, you know what? It’s over. You know, we, we don’t have to live like that anymore. Uh, and it was amazing. You know, and I- and I- I had came home and I had handed her the deposit slip. And I don’t think she believed it at first. And when you see tears in your wife’s eyes-

Jim: Mm.

Brian: … you know, because of the power of the journey. I mean, that’s four years of scraping and pointing and wondering if it was going to happen. When we began all of this, we thought it was gonna take 15 years. Uh, you know, $127,000 is a lot of money.

Jim: Yeah.

Brian: Uh, especially when you still have your day-to-day bills that you’ve gotta pay. You still gotta pay for health insurance. You still gotta pay for, you know, your house and, and other living expenses, your utilities. Uh, and it was done. It was over. And we knew this new chapter was going to begin. And, and we, we celebrated right there in our kitchen.

Cherie: We did. And it was such a sense of relief. And I did collapse into tears in Brian’s arms. And then we frantically cleaned one corner of our kitchen up. And we wanted to share that moment with the greater community that had supported us. And so we YouTube’d ourselves paying the last of, um, debt and paying off that Sallie Mae bill. And the last student loan that we had. And it’s still out there on YouTube. And it’s had lots and lots of views of other people, just as a way to say thank you and to encourage other people and to just capture that moment. If you see the picture on the front of the book, we had a friend come over and take pictures that day. And I don’t think we could recapture those expressions on our faces. Those are the looks that you have when you spend four years paying $127,000 in debt off. And he just offhandedly said, “That stack of bills-” which are actually all of the bills that we had paid off, we would put them on the refrigerator after we paid them off and write the date on them, those are the actual bills that we paid off. And we threw them up in the air. And I am so thankful that he caught that moment on camera for us forever-

Jim: That’s a great picture. Right on the cover. Okay. I’m sitting here. I’m, uh, driving down the road. I’m thinking about this, my spouse, this is something I’ve been wanting to talk to her about for months. And we do have some amount of debt. I’m worried about it. We’re stretched so thin. What would you say to me?

Cherie: Start with love and remember why you walked down the aisle. And I always tell people, you are on the same team together. And there was a reason why you chose each other. And there was a reason why you stood in front of God and your friends, and your family and you said, “I will cherish you.” And that is the most important thing. Money is not the most important thing. Getting out of debt is not the most important thing at all. But if you begin there, I think your heart’s more prepared to communicate a message. And then secondly, um, that casting that vision. That just really grabbed my heartstrings and said to me, you know what, this might not be possible but what if it is?

Jim: That’s well said. That is so well said. Look to the future. That vision is what I’m hearing from you. You had hope. Um, this is Brian and Cherie Lowe, the book Slaying the Debt Dragon. This has been a great discussion. Thanks for being with us.

Cherie: Aw, thank you so much.

Brian: Thanks for having us.

John: What a great reminder about the need for good communication in marriage, uh, to work hard and to seek God’s guidance as you pay off debt. And then with His help achieve a life of financial freedom. Uh, to that end, the Lowe’s book is a must read. It really, uh, provides dozens of debt slaying strategies to help you. You’ll find that book and a CD or instant download of this two-part conversation at focusonthefamily.com/broadcast.

Jim: John, here at Focus we hear from so many couples who are really struggling in this area of finances. It’s one of the top responses we receive. Uh, one’s a spender and one’s a saver. Or neither are savers and things get out of control. If you’re at a point where your relationship is fractured and you need to talk to someone, please know that we have caring Christian counselors right here on staff to talk with you. Uh, call to set up an appointment or they can refer you to someone in your own area for help. And then here at the close of the program, for those who are capable of helping us, let me invite you to support the ministry of Focus on the Family. Together we can help marriages and help save baby’s lives and so much more. We’re helping literally hundreds of thousands of couples to build stronger, healthier, more God-honoring families. But we need your help to continue in that mission. Uh, no donation is too small and today, with your donation of any amount, we’ll send a copy of Slaying the Debt Dragon as our way of saying thanks for joining our support team. And if you need the resource and you can’t afford it, we’re gonna trust others will take care of that. So just call and ask for the book and we’ll gladly send it to you.

John: Well, uh, contribute as you can or, uh, simply request that book when you call 800, the letter A, and the word FAMILY. Or again our website is focusonthefamily.com/broadcast. On behalf of Jim Daly and the entire team here, thanks for joining us today for Focus on the Family. I’m John Fuller inviting you back as we once again help you and your family thrive in Christ.